The 176th Ordinary Meeting of the OPEC Conference (6th OPEC and non-OPEC Ministerial meeting) Vienna, Austria, 1st July 2019

After much deliberation and discussion, over when to meet, from April to late June to early July, OPEC and its non-OPEC partner Russia finally agreed the date but under the direction of Russia.

The first news that the group would extend the cuts of 1.2mbpd for a further six to nine months did not come at the end of the OPEC gathering but from the G20 Meeting at Osaka two days beforehand with the announcement being made by President Putin of Russia!

Following on from the G20, it was subsequently confirmed today that it would officially be extended for nine months until the end of March 2020. However, there did appear to be some frustration from OPEC members that the decision should have been made by OPEC, not Saudi and Russia, and that the announcement should have come from OPEC and not from a non- OPEC source.

It was no surprise that the news was already in the market early today, before any formal announcement from OPEC and, with that, the oil price moved up. In my view, as of now, this will probably be a short-term reaction as with further oil supplies coming to the market, certainly based on the IEA forecast, we can expect prices to be under further pressure unless OPEC cuts further.

I have always believed that Russia would never be party to anything that it was not able to control, and today, having supported OPEC for two years and held the peace between Iran and others, particularly Saudi Arabia, Russia has not only taken over the timing of the meeting but also the outcome. Without Russia and other sympathising non-OPEC producers, Saudi would have lost control and OPEC would have failed in the face of rising US output, increasing the pressure on OPEC to cut its output and in so doing, see its market share diminish.

The plan was later ratified by the OPEC members, to roll it on until the end of March and review then, at a time when the weather is easing and demand not quite so critical. It would also give OPEC more time to think about a longer-term strategy if any. The US has put another 4mbpd into the market, forcing OPEC+ to pull back and balance the market.

In effect as others increase market share, OPEC+ decreases and this they cannot allow to continue. Therefore, a long-term plan is urgently required to involve the US too. Similarly, as the pressure mounts, President Trump expects OPEC+ to keep prices low to ensure cheaper gasoline in the US in the run-up to elections next year.

In spite of this concern, Khalid Al-Falih, the Saudi Minister, casually explained that they would be monitoring the situation almost as if they didn’t believe that US shale production was long-term.

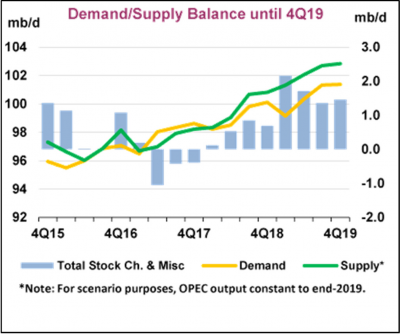

In the short-term, though, there is a view that supply will exceed demand, and this is clearly illustrated in the adjoining chart from the IEA.

Since the start of the partnership between OPEC and non-OPEC, the oil price has been maintained at a reasonable level for both consumers and producers, although, when balancing the budget, some producers seem to assume that their budgets are a true representation of the value of their oil.

Yet, whatever their aspirations, there is a market price, and that will probably roam in the $60-70 range depending on geopolitical tension and trade wars, which will ultimately impact on the state of the global economy.

At the last meeting back in November, I had intended suggesting that OPEC should consider holding meetings more frequently than every six months and I was excused from this when they announced that the next meeting would be in April. That seemed to make sense and there would be little chance of the market running away from them as it had during the last six months of 2018. However, when the monitoring committee, the JMMC, reported back that the overall cut of 1.2mbpd had worked well, with supply and demand back in balance, they took the very unexpected decision to postpone the date of the meeting from April to June.

For OPEC, the good news came on 19 May when the JMMC which confirmed the Declaration of Co-operation between OPEC and non-OPEC or Saudi and Russia was working well and that with monthly compliance average 120%, the market was balanced. Of course, much of the cuts were the result of cuts from several OPEC Members whose output was restricted anyway, supported further by cuts from Saudi Arabia.

The decision to roll on until a later date was an easy one. Nevertheless, with OPEC Meetings scheduled in advance, it has always been beneficial to plan ahead, knowing that there was a schedule in place, ready to act if any corrective action was required.

As we got closer to June, less than a week away from the Meeting start date of 25 June, OPEC was still wavering on which date to use. It seemed that they had moved on from 25-26 June although hadn’t yet advised anyone. As further dates were being circulated, Iran supposedly refused to comply, and it seemed for a while that the meeting scheduled for 25-26 June would actually happen. Then Alexander Novak the Russian Minister visited Iran and from the discussion that took place,1-2 July dates were accepted and quickly announced. What was perhaps not evident was that decisions to change the dates were coming from Russia and not OPEC.

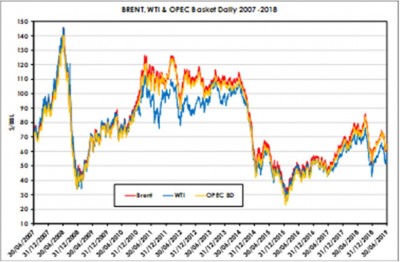

Meanwhile, the price of oil gently simmered at the lower level of just over $60 for Brent and $10 less for WTI at just over $50, in spite of the earlier attacks on several tankers in the Gulf of Oman.

The US immediately blamed Iran, although what was also surprising was that the tankers were supposedly heading for Japan and Prime Minister Abe of Japan was on a visit to Tehran at the time. One has to wonder why Iran would insult such a dignified visitor in this way. Proof was and still is lacking, although conjecture is not.

There has been much dialogue in recent weeks primarily around concerns of the anticipated slowdown brought about by the trade war between the US and China and its implications for Asia as a whole, with overall geopolitical tension centred on the US-Iran tension.

Looking ahead, it’s difficult to know what the long-term strategy might be. Saudi and Russia, plus other OPEC and non-OPEC countries have benefited greatly from this co-operation and although individuals may want to see a higher price, they have to recognise that a higher price will hit demand, and with the threat of a global slow down possible, a higher oil price would not be sensible. Furthermore, it would encourage greater production from other sources and further moves away from fossil fuels. Climate change is very much on their minds!

So, where the market is is probably good for all parties for now. It is certainly good for the US shale market, which has added around 4mbpd to world oil supplies, and with some taken up by increased demand, the balance has had to come from the cuts lead by Saudi and Russia and will continue until there is some level of resistance.

For how much longer can they tolerate a market in which they are forced to accommodate the new supplier, the US? It’s inconceivable that they will defend the price by simply cutting output to accommodate more from the US, and this is the question that has to be answered particularly as supply will probably exceed demand if OPEC continues output at current levels.

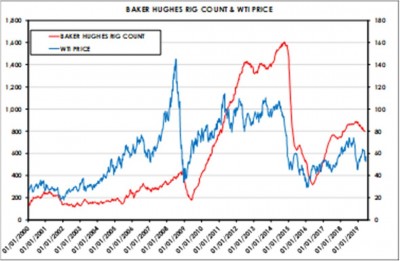

In the last couple of years since OPEC undertook the more aggressive stance to control the market, the US rig count has increased and over time built up a sense of stability.

Russia is not a member of OPEC, but as the largest by far of the non-OPEC countries that support OPEC, its support is paramount and now to the extent that it has strong influence within the OPEC membership.

So, once again, the cut of 1.2mbpd will be maintained, primarily by Saudi Arabia. Russia, although a party in principle to the agreement will have some difficulty in maintaining cuts, but for the sake of maintaining the so called Declaration of Independence, which should have been signed in April and still remains unsigned, it will continue to give moral support to OPEC and Saudi while the rest of the OPEC entourage will follow on. As part of this Meeting, the formalisation of the agreement was on the agenda.

Geopolitical tension is rife not only within OPEC and non-OPEC but across the Middle East and Asia. The impact of the US-China trade war is being felt across the world in all. However, President Trump is back on negotiating with President Xi Jinping, and perhaps this will calm down the tension but only until a settlement has been reached. The tweets are flowing but that’s not enough. A tangible settlement must follow.

Likewise with North Korea where he has again met with the Presidents of both the North and the South. Whether President Kim Jong-un of the North will be prepared to give up the so- called nuclear weaponry that he has developed over the years together with long range rockets is questionable.

Nevertheless, the country needs support, and the US is in a position it to give it if it chooses, alongside China. It will not be a simple once in a lifetime deal making process, as cultural differences will need to be accepted and understood.

Further afield, Middle East peace is even further removed with the recognition by the US of the whole of Jerusalem as being part of Israel. Without the creation of a state for the Palestinians and the removal of settlements in Gaza, there cannot be a peace agreement. The recent cartoon in the Financial Times by Ingram Pinn “Deal of the Century” summarised the situation precisely with the image of Jared Kushner unfolding the rolled-up plan “The Trump Peace to Prosperity Plans” and sweeping the Palestinians away underneath. Years ago, the importance of this settlement was of paramount importance to development in the Middle East, but today, those countries that used to support the Palestinian cause have faded away. As a Palestinian journalist friend told me today “it’s all over for Palestine”.

For Iran, the situation is particularly serious as sanctions are crippling the country as President Trump intended, the objective being to break the ruling administration down, forcing it to crawl back on its knees to seek whatever it could. Most countries will protect their sovereignty to the very end, and Iran is a very proud nation having suffered much hardship since the revolution in 1978.

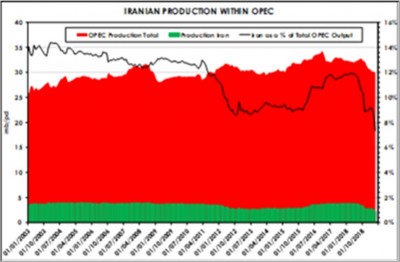

The impact of sanctions on Iranian oil output can be seen in the adjoining chart and day-by-day as the threat of retribution against those that are prepared to trade with Iran, the output dwindles further.

For OPEC, it’s down to other members to make up the loss not only from Iran but from Venezuela, also suffering sanctions from US, but in Venezuela one can argue that sanctions are justifiable although one does not know what the end plan is or even if there is one.

The Nuclear Agreement with Iran was signed in 2015 by the UK, France, Germany, China, Russia, and the US. All parties were happy with the deal, including those involved from the US. I spoke to friends at the International Atomic Energy Authority at the time who told me that the Iranians were fully compliant, answered all questions, did what they were asked to do, and allowed access to all sites that needed to be visited. There were no apparent issues.

President Hassan Rouhani of Iran is a “moderate” and was keen to engage more with the West. Iran needs to buy goods and services, and this was evident as soon as the agreement went through. Meanwhile, President Trump has pulled the US out on the basis that it was “the worst deal ever” and has since talked about many issues as being the reason, other than those related to the Nuclear Agreement.

In response, Iran announced the resumption of nuclear enrichment and today, coincidently, the IAEA announced that Iran has breached the enriched uranium limit agreed under the terms of the agreement. For Iran to halt the programme, it would want the remaining signatories to honour the agreement and continue to trade with Iran.

A non-dollar financial channel has been set up for the countries to trade with Iran but, in face of retribution from the US, most, excluding China, are reluctant to use it. With Iran facing further stress through losing its market share within OPEC, further tension will follow with Saudi Arabia, which is supporting and encouraging the US in its sanctions against Iran.

During the day, I managed to speak to a couple of ministers, Dr. Diamantino Pedro Azevedo from Angola and Jean-Marc Thystere Tchicaya from Congo, who joined last year. For Angola, with an output of 1.8mbpd, he is happy with this level in compliance of the OPEC directive; the consortium is working well with support from Russia. He is in agreement with the plan to extend the cuts, certainly to the end of the year and longer. In terms of the impending supply overlap, he was not concerned, maintaining that he is able to sell all the product that he produces.

I moved across then to talk with HE Jean-Marc Thystere Tchicaya of Congo. His country is currently producing 350,000 barrels per day and as a new member of OPEC seems happy the organisation and he would have come in on the strength of the Russian co-operation with OPEC.

Unfortunately, my French was not good enough to converse directly with him, so we had to communicate thorough his OPEC Governor. Nevertheless, his positive views replicated those of Dr Azevedo. On the other side of the room, the Saudi and Iranian desks were literally so over-crowded that they were hidden from view. The two that I spoke to may be small players, but they usually detect trouble elsewhere and each seemed relaxed about the day ahead. I did at least manage to get a friendly wave from one of the Iranian delegates but was unable to get close to talk.

At the end of the day, the press conference took place and Manuel Quevedo Fernandez the Venezuelan Minister and OPEC President personally confirmed the extension of the programme to maintain the cut of 1.2mbpd until March and then passed on to Khalid Al-Falih, the Saudi Minister and Chairman of the JMMC, which monitors output performance from each member. He said that the world economy was looking stronger this week than last due to the “agreement” between President Trump and President Xi of China, although all that seemed to have happened was that some kind of truce had been agreed over US firms supplying Huawei as a pre-cursor to setting up resumption of discussions regarding an actual “trade deal”.

He went on to say how carefully OPEC+ members were being monitored and liaised with him to maintain compliance. They would also be monitoring global stock levels in the hope that they would return to 2010-2014 levels.

He explained that, contrary to views displayed in the media that there was 100% consensus in OPEC for the partnership with non-OPEC and the Charter to be signed to formalise the Declaration of Co-operation. The conference had been delayed by several hours and the view on the outside was that reaching agreement across all members was experiencing difficulties over agreement on the Charter, which Mr. Al-Falih denied.

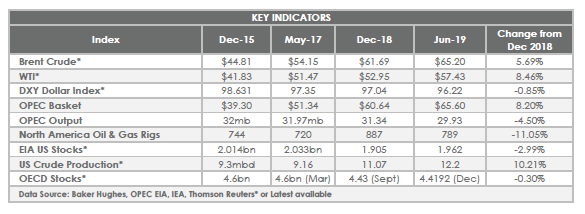

We again have set out below the key statistical pointers that have emerged from OPEC decisions in recent years. These are the factors that determine their future success or failure.

Where will the price of it all go? The figures in the table below set out the results from the Reuters poll conducted at the end of May. The top line is for today the most realistic, while the lower and higher ranges represent the impact of geopolitical events that may occur.

As I have implied before, looking ahead, there are many contentious geopolitical and trade issues to consider and as these are all ongoing, it’s difficult to know what to expect.

At the top of the list, we must have the US-Iran and the US- China situations with Korea close behind. Then, for OPEC, we have to look at the output of oil from the US and elsewhere and with global output slowing and Mr Al-Falih expecting soft demand, I shall leave you again with my favourite cartoon kindly provided by Joe McMonigle of Hedgeye Risk Management which for now, says it all.

Until next time, if you would like to discuss anything with me personally, please get in touch: John Hall, John.Hall@alfaenergy.co.uk + 44 7785 274530